Most people, once they’ve been involved in an accident and they come in for a consultation, they bring in their policies or they don’t. Either way, it’s totally fine because under the law, their insurance company has to give it to us.

The first thing that we go over with our clients is the insurance policy because most people don’t have any idea what is on their auto insurance policies and what those things on their policies actually cover.

In this blog, I will to go over that in details so, you can be educated and have a better idea of what is going on, on your auto insurance policy and if you don’t have these things on the policy, it’s better to know now so that you can be properly covered before something happens. After you’ve been involved in an accident, you usually have at least three claims going at the same time.

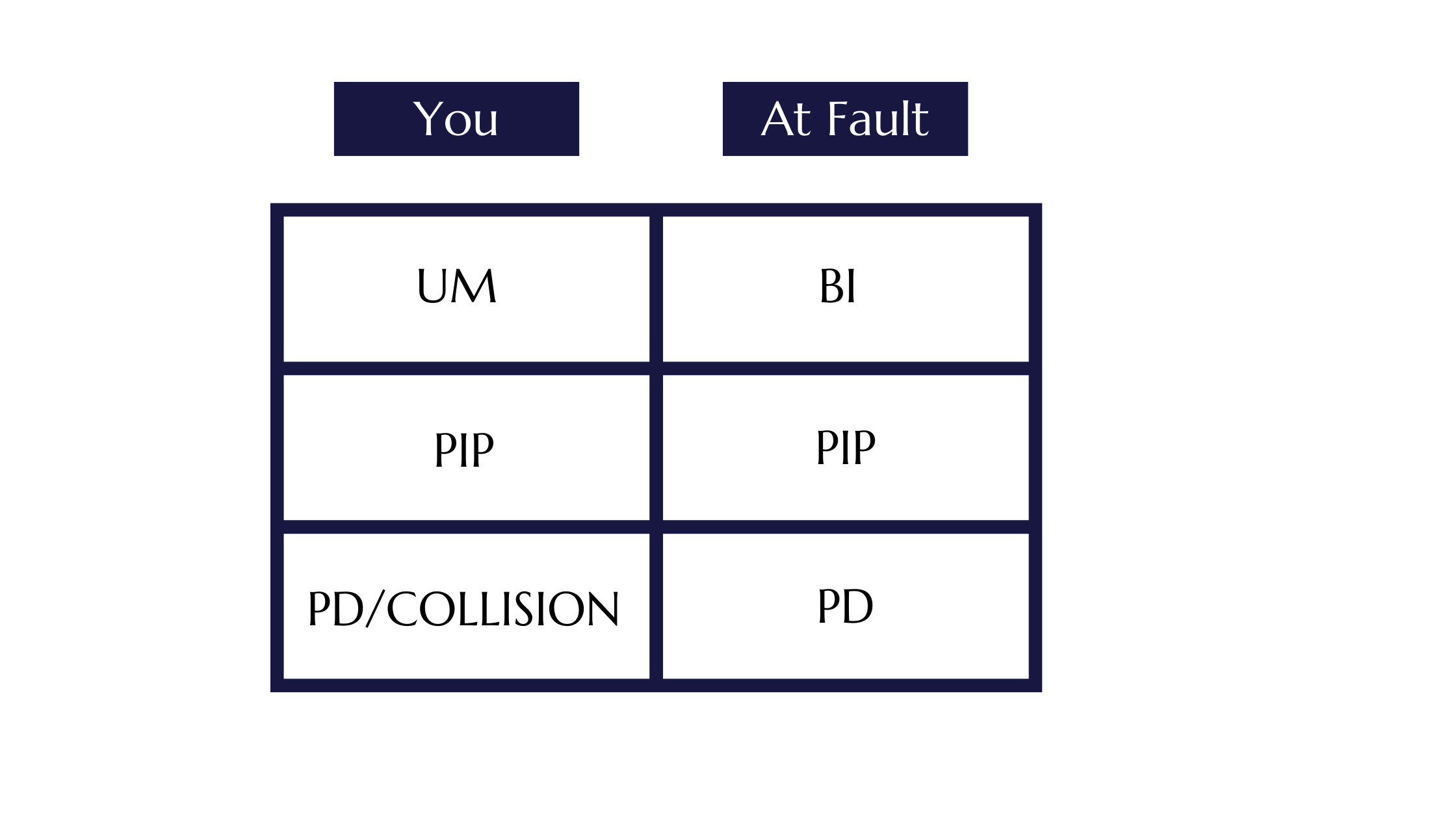

So, in the chart above, the left side is going to represent you and your insurance company and the right side is going to represent the other party, the at fault party and their insurance company. The first thing that we need to know in the state of Florida, a lot of people have the misnomer of full coverage. Full coverage is a variety of things. What a lot of people tend to think is full coverage is actually legal coverage.

Legal coverage is your PIP and your property damage.

PIP is your Personal Injury Protection, sometimes known as no fault benefits, and your PD or your Property Damage is that portion of your policy that actually goes to fix or repair damages you may have caused to another party’s property, not your own. So, as you can see, these have two different things because you need to have the property damage on your own policy but your property damage is not what is going to cover your vehicle if you are involved in an accident, and we’ll go into that in a little bit.

The first claim that we need to look at is the property damage.

The second claim is going to be for your PIP which is for your your medical benefits.

And then UM & BI is where you actually the purpose of hiring an attorney in where you would be getting your compensation or your benefits from if you are injured in an accident.

The first thing that we need to go and look at is whenever we’re involved in an accident, there’s going to be two facets of it, the liability, which is the who’s at fault part and then after that is determined we shift over to the damages portion. Damages is a whole other animal that we’ll get into later. But when we’re dealing with the property damage, right, the damage to your vehicle or any contents within your vehicle, a lot of times people are rear-ended and they’ve got things that are inside of their trunk that also get it damaged. That falls into this category as well.

So let’s say there is no issue as far as the liability or the who’s at fault. That means the at faults property damage portion of the policy should be paying to repair your vehicle or total it out. Keep in mind, in the state of Florida, this is only a policy of usually up to $10,000. In this day and age, that doesn’t really go very far. That’s why you need to make sure if it makes sense financially for the value of your vehicle that you also carry collision on your vehicle.

Let’s say that the at fault portions insurance company has not accepted liability or they’re claiming that you are partially responsible for the crash. Their PD will not pay for the entire $10,000, they might only pay a portion of it. So you’d be wanting to go under your own policy and going through that portion of collision.

Now if you don’t have collision and they either don’t have an active policy or they’re claiming you are at fault for this crash, then they will not be paying to repair your car. So you will be out of pocket here if you do not have collision.

Please check your policy.

The next thing that after you’ve been involved in an accident, you need to figure out were you injured? If you are injured your PIP, which is your personal injury protection, like I said, the no fault benefits that is up to $10,000. Now, regardless of whether or not you have health insurance, your PIP in the state of Florida is your Primary Health insurance.

If you’ve been involved in an automobile accident, you do not get access to the at fault parties PIP, only your own PIP. That’s why it’s called personal injury protection. So, personal injury protection or your PIP benefits can pay for your medical bills, any kind of treatment afterwards and any diagnostic testing, if you need prescriptions, they will do a portion of reimbursement. It will also reimburse mileage. It can reimburse household help. So if you needed to hire somebody to clean your house or to mow your lawn, those types of things come out of PIP. But keep in mind it’s only up to $10,000. As you can see that goes very quickly, especially if you’ve had a visit to the ER. The other thing that I want to mention about PIP is that you have to have sought medical treatment within 14 days of the crash in order to still get these benefits.

If you do not seek treatment within the first 14 days after a crash, your own insurance company could reject the coverage and not give you that $10,000 worth of PIP benefits.

The most frequently asked question I have as far as PIP is why do I have balances? Well, your PIP is only going to pay your medical bill at 80%. Now there are different coverages that you can purchase like Med pay and obviously if you have health insurance that will cover the remaining 20% but for purposes of just PIP coverage It is going to pay a medical bill at 80%.

What that means is if you go to the hospital and your bill is $1000, that means your PIP is going to kick in $800 and leaving you $200 or 20% of the bill. That’s going to be your responsibility even if you were not at fault for the crash. What that means is, that we look to see whether or not the at fault party have BI (Bodily Injury coverage) on their policy and we say hey at fault insurance company, but for the negligence of your insured, I want to have this 20% balance you need to pay me. Obviously 20% is just the bottom of what you’re legally entitled to as far as compensation. However, for the purposes of this blog and as a general conversation, we’re just going to go with this example.

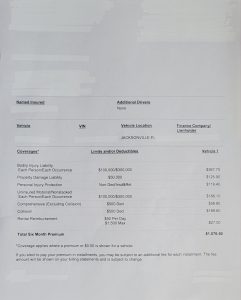

When we’re looking at BI and this is a good time to actually look at the policy. So we can see whether or not they have BI coverage.

Now, it doesn’t matter. Again, we’re not looking at BI on your policy. We are only looking as far as the at fault. And just like they can do with the property damage, if there is any kind of issue as far as potentially a liability issue or comparative negligence, meaning they’re finding you to be a portion at fault, then that percentage as far as what the amounts available to you could change.

But what we’re looking for is whether or not they have BI because in the state of Florida they are not required to have it. It is not mandatory. So whether or not they have bodily injury coverage, we have to consult the declaration page from the insurance company. These tend to come In policies If they do have it, the minimum is 10,000/20,000 , 25,000/50,000 or 50,000/100,000. That’s what it would look like on your policy.

What that means is any one claimant can get up to $10,000 or all claimants would be splitting 20,000 pro rata for their injuries. So what that means is, let’s say you are alone in your car and you were involved in a crash with someone who is also alone in their car. Well, there is no issue there. We know if there’s a 10/20, the most you could get would be $10,000, but let’s say you were alone in your car but the at fault driver had a passenger or let’s say 2 passengers. So in that case any one of us bringing a claim because the at fault driver having passengers, those passengers potentially have a claim against the at fault driver, right? They had no negligence because they were just involved as passengers. So that means they too are entitled to bring a claim. And what that means is, any one of us could get up to $10,000, or all three of us could be splitting $20,000.

Like I mentioned before, bodily injury is not required in the state of Florida. So if they do not have BI or they don’t have enough BI, if your injuries are in excess to the amount of their coverage, we would go over UM (Uninsured Motorist) and look to your own coverage to see if there is zero BI or under insured motorist if the policy limits for BI are not enough to cover your injuries so therefore you could make a primary UM claim if there’s no BI or a secondary UM claim If there is BI but the the limits are not enough to cover your injuries.

I hope this blog helps you better understand your auto insurance policy. If you or your loved ones were involved in an accident, please contact us for a free case evaluation.

Disclaimer: The content of this blog does not constitute legal advice. Use of the Internet or this website for communication with our firm, or any individual member of the firm, does not establish an attorney-client relationship. Confidential or time-sensitive information should not be sent through this website.